Decreasing Your Credit Card Limit NOW!

In such turbulent times, many credit card holders want a higher credit card limit for a lot of reasons.

Credit cards have grown to become the Best Alternative cash for daily consumables, and this trend is very much in line with the National Payment Policy, which is aiming for a Cashless Society.

Most of us now know the benefits of using credit cards as an alternative to cash. Imaging carrying $5,000.00 cash to buy a Personal computer, Furniture, Jewellery etc. On top of that, you get cash rebate too.

Credit cards is NOT for everyone especially those who got NO good financial discipline like not paying credit card outstanding amount in full every month. Maybe debit cards is more suitable for this group of people.

A lot of Banks are aggressively promoting personal loan and credit card by giving automatically higher credit card limit. Just ask yourself how many Telemarketing calls you received per month for promotion on supplementary card, personal loan and balance transfer program. The banks are generally thrilled to give you an increase in credit limit, if they think you will use it wisely and would not go bankrupt.

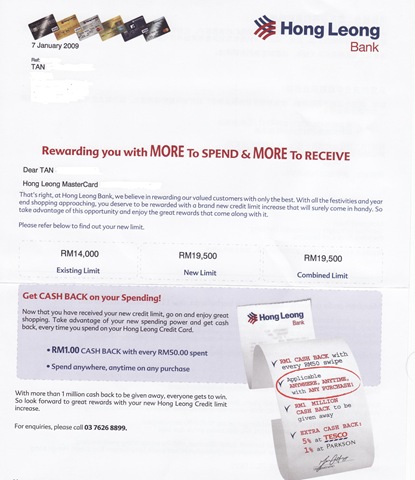

Look what I got in the mail today! Almost reached Platinum card member credit limit 🙂

And always remember, a higher credit card limit means greater purchasing power, but it also increases the risk of your having to pay greater interest charges and other processing and late fees if you have difficulty repaying the higher balances.

If you find yourself getting deeper and deeper into debt hole consider lowering your credit card limit. Just ring up the credit card company and ask them to decrease the limit on your credit card. This way you can still have the convenience of a credit card but you will have some safe guards to help keep you away from going deep into debt hole.

Of course, the best way to use a credit card is to pay off the balance at the end of each month in full. With a lower credit limit, it will be easier to pay off the balance. If the maximum you can charge on your card in a given month is $1,000, that will be a lot easier to pay off than $10,000.

By intentionally controlling your credit card limit, you can set yourself up to be Financially Free. Keep in mind that the banks make lot of money when you are in debt, so they are going to try to give you as much credit as possible.

Since they make money when you are in debt, don’t consider the credit limit increase!

Please help me to jump out from the deep hole of debts from credit card.. I have a 11,000 debts but The problem is even i pay in 10% also remain the same outstanding balance:-S could somebody guide me about this problem and solve it as soon as possible?

May you wanna get help from Agensi Kaunseling Dan Pengurusan Kredit (AKPK)http://www.akpk.org.my

AKPK is an agency set up by Bank Negara Malaysia in April 2006 to provide financial counselling and debt management to individuals as well as financial education to help individuals take control of their financial situation and gain peace of mind that comes from the wise use of credit.

Donald,

As I am working in a credit card company, my advice is one way to reduce the credit card debts and interest is to borrow personal loan with extended time frame in order to cover ur debts.

Credit card interest 18% p.a. Personal loan as low as 7.5% p.a.Take up a $10,000 personal loan with 5 years repayment scheme, every month pays $230. The interest is fixed and stop using ur card now.

Yes..get help..while restructure your debt. Please don’t incur any new credit card debt!

Increase of credit limit may not necessary bring a Good news!

Issues with credit limit

—————————-

WHILE the debate on the RM50 service charge on credit cards rages on, few people pay attention to the changes to their credit limit.

Last year, when applying for a credit card, I clearly stated my choice of a Classic card. My first surprise came when I received a Gold card instead. I called up the card centre and was told that I qualified for a Gold card.

Though I am appreciative of the kind gesture, this is clearly a blatant disregard of my rights as an individual. A letter requesting a change in card choice or a phone call to seek consent from the applicant should have been the proper procedure.

This is a serious issue because it relates to the credit limit that different card types (Classic, Gold or Platinum) offer. Not needing so much credit was one of the reasons I chose a Classic card. The Gold card that was given to me had a credit limit of RM10,000 before I asked for it to be reduced to RM6,000.

My second surprise came recently when upon checking my credit limit in my statement of account I found that it had gone up to RM11,000. Again, upon checking with the card centre, I was told that most likely a notification was sent out but had not reached me.

A notification? I start to ponder if the card issuer has the right to change my credit limit automatically.

I was given various excuses such as it was a decision from the top management or that it was done through an automated system.

I asked if my card was lost or stolen and someone had used up my credit limit, would the card issuer pay for the RM5,000 difference that I did not authorise for?

The answer was no, the card holder would be held responsible. If the holder is answerable for the credit limit, wouldn’t he have every right to be in control of the credit limit?

I was further told that I can only reduce my credit limit to RM7,000 for a Gold card and if I wished to reduce it further I would have to change my card to Classic.

Although my problem has been amicably resolved, such regulations should not have been imposed.

While the eligibility of card types may correlate with the income of an applicant, once a credit card type has been approved for an individual, he should be given the flexibility to re-adjust the credit limit at any given time.

This will give the card holder a sense of security as he will be in full control.

For example, in times of hardship, a person may choose to reduce the limit significantly to curb overspending, or when one is travelling one may choose to increase the limit.

BENNY TEH,

Penang.

from:thestar.com.my/news/story.asp?file=/2010/1/4/focus/5406117&sec=focus